Many employers in the U.S. often find the tax obligations of their J-1 visa employees to be a challenging area to navigate.

With so many forms and information needed with each employee, there is no surprise that some employers find the process of tax withholding for J-1 visa students tricky. This, coupled with the fact they will not be a resident for tax purposes, make it more challenging.

The need to complete all of the forms correctly cannot be underestimated, as every nonresident needs to abide by U.S. tax law.

In this guide we will examine the key tax information that U.S. employers need to know when employing J1 workers.

Can I hire someone with a J-1 visa?

In short, yes – if a J-1 worker is eligible, you will be able to hire them.

The J-1 visa is a non-immigrant visa that offers cultural and educational exchange opportunities in the United States. J-1 Exchange Visitor programs include au pairs, summer work travel, interns and trainees, high school and university student exchanges, physician exchanges and more.

Individuals on a J-1 visa will have to find a J-1 visa program sponsor. J-1 visa sponsor is an independent organization which sponsors the J1 visa. Then, they can work for a specific company or organization.

Once the J-1 worker is sponsored, they will be available to hire by the host organization once their visa is fully verified.

As a J-1 visa host company you are most likely to work with J-1 visa interns and trainees or J1 seasonal workers (J-1 Work & Travel visa).

Difference between a J-1 visa intern and a trainee

The main differences consist in the employee’s educational status and the duration of the visa.

J-1 visa interns are college or university students or recent graduates with no prior work experience. The visa is issued for 12 months plus an additional 30 days to travel the U.S.

The J-1 visa trainee program on the other hand is intended to allow foreign professionals (who have a certificate, degree, or equivalent work experience) to gain exposure to U.S. culture and to receive training in U.S. business practices in their chosen occupational field. The visa is issued for up to 18 months plus 30 days to travel the U.S. but not work.

Employment of J-2 Dependents

The J-2 visa is a non-immigrant visa issued to spouses and dependents (unmarried children under the age of 21) of J-1 visa holders who accompany or later join the J-1 participant in the United States.

The J-2 dependent spouse of a J-1 visa worker may apply to the U.S. Citizenship and Immigration Services (USCIS) for employment authorization.

Also read: Comprehensive Tax Guide for J-2 Visa Holders

Residency for tax purposes

Are J-1 participants residents or nonresidents for tax purposes?

One of the primary deciding factors in evaluating how a J-1 worker should be taxed is the determination of their residency status for tax purposes.

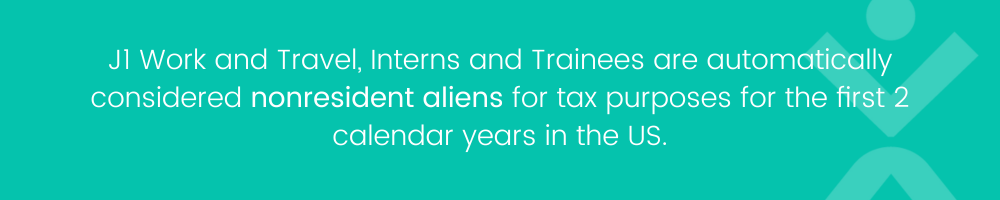

It’s important to note that the IRS deems that the majority of J-1 visa holders are nonresident aliens for tax purposes.

J-1 Work and Travel, Interns and Trainees are automatically considered nonresidents and exempt for the first 2 calendar years in the U.S.

If a J1 visa holder has been in the U.S. for longer than two of the last six calendar years, the Substantial Presence Test will determine their correct tax residency status.

J-1 visa holders can determine their tax residency status for FREE using Sprintax.

Do J-1 participants pay tax in the U.S.?

Yes. As nonresidents in the U.S., J-1 workers are taxed on:

- Any income that they will earn from employment in the U.S.

- Any stipend, fellowship, grant, or award they receive

- Any other income from U.S. sources that they receive

Depending on where the participant chooses to carry out their employment, they may pay up to 4 different types of tax on their earnings. These include:

- Federal Tax

- State Tax

- Federal Insurance Contributions Act (FICA) Tax

- Local Tax

Social Security and Medicare tax (FICA)

FICA is imposed at a combined rate of 15.3%, comprising Social Security and Medicare taxes.

Certain nonresident employees are exempt from FICA withholding.

FICA taxes withheld in error

In general, J-1 workers should not be charged FICA tax. If FICA is deducted in error, they are generally entitled to apply for a refund of the amount paid.

Generally, FICA taxes withheld in error happen after an employer incorrectly files Form W-2.

If FICA taxes are withheld in error, the employee may be due a FICA tax refund.

You will be able to secure a FICA refund for your employee by correctly filing a Form W-2C, formally known as Corrected Wage and Tax Statements.

Sprintax can also get FICA tax refunds for nonresident aliens. In fact, we have facilitated over $12.5m in FICA tax refunds to nonresidents.

Tax treaties – what employers with J-1 visa employees should know

J-1 visa holders can claim tax treaty benefits

The U.S. has tax treaties with over 67 countries across the globe that allow nonresident aliens on J-1 visa to receive either exemption or lower rates of tax in the U.S.

This means, if your J-1 employee is from one of these countries, they may be entitled to benefit from a lower rate of tax.

Whether or not a J-1 participant is entitled to tax treaty benefits will depend on several factors, including:

- Their visa type

- Their income type

- What work they are being compensated for

- Their duration of time in the U.S.

The U.S. has tax treaty agreements with each of the following countries:

| Armenia | Australia | Austria | Azerbaijan | Bangladesh | Barbados |

| Belarus | Bulgaria | Canada | China | Cyprus | Czech Republic |

| Denmark | Egypt | Estonia | Finland | France | Georgia |

| Germany | Greece | Hungary | Iceland | India | Indonesia |

| Ireland | Israel | Italy | Jamaica | Japan | Kazakhstan |

| Korea | Kyrgyzstan | Latvia | Lithuania | Luxembourg | Malta |

| Mexico | Moldova | Morocco | Netherlands | New Zealand | Norway |

| Pakistan | Philippines | Poland | Portugal | Romania | Russia |

| Slovak Republic | Slovenia | South Africa | Spain | Sri lanka | Sweden |

| Switzerland | Tajikistan | Thailand | Trinidad | Tunisia | Turkey |

| Turkmenistan | Ukraine | Venezuela | United Kingdom | Uzbekistan | Belgium |

How can a J-1 employee claim a tax treaty benefit?

If your employee is entitled to claim a tax treaty benefit, you should advise them to prepare forms 8233 or W-8BEN, depending on what they are claiming.

With Form 8233, this should be completed right before the employee starts the job, ensuring it is submitted before their first paycheck.

If a foreign national receives certain other income in the U.S., they must also fill out form W-8BEN. This income includes:

- Scholarship/Grant

- Interest

- Rents

- Dividends

- Premiums

- Royalties

Sprintax Calculus Tax treaty engine

The correct determination and application of tax treaty benefits to employee paychecks is particularly challenging.

And exactly how these treaty agreements are applied depends on the circumstances of each individual employee.

Sadly, there is no ‘one-size-fits-all’ approach that can be taken and looking up tax treaty articles via IRS website can take a very long time if you’re not sure where to look for this information!

With that in mind, Sprintax Calculus has a comprehensible Tax Treaty Engine within our Tax Determination System.

This is an invaluable tool in the identification of potential tax treaty benefits for your nonresidents.

To identify if there is a tax treaty available, all you need to know is the correct income code and country of residency for the relevant employee/nonresident.

Once you enter this basic information, our Tax Treaty Engine will provide you with an outline of whether there is a potential tax treaty available to them, as well as including the article, limit and time period involved.

We will also direct you to the specific passage of the treaty agreement, should you require any further information.

Book a Demo for Sprintax Calculus

6 J-1 visa rules for employers: key steps to employing J-1 workers

- Prior to the beginning of employment, ensure the workers have applied for their SSN (Social Security Number) or an ITIN (Individual Taxpayer Number) if they are not eligible to apply for a SSN.

- Use the Substantial Presence Test to determine the tax residency of the worker

- Determine their income type

- Identify if the worker can apply for tax treaty benefits

- Obtain and file all the necessary tax forms

- Ensure that the worker receives the correct documents at the end of the tax year.

Key tax forms J-1 employers need to know about

Form W-4 – a key withholding form for employers hiring J-1 visa workers

Form W-4 (Employee’s Withholding Allowance Certificate) is used by payroll to calculate federal income tax withholding for J-1 visa employees.

Each J-1 participant must complete Form W-4 accurately when they start working to ensure withholding is calculated correctly and in compliance with IRS rules.

How to fill out a W-4 form for a nonresident employee

For nonresident aliens, the following steps of Form W-4 are relevant (Steps 2, 3, and 4 are generally not completed by nonresidents, except in limited cases such as students and apprentices from India):

Step 1. Enter Personal Information

This includes name, address, date of birth etc. There’s also an option to file as single or married filing jointly – this can affect tax rates for the employee. Check the “Single” marital status on Step 1 (c) (regardless of actual marital status)

Step 2. Multiple Jobs or Spouse Works

This is only relevant to the J-1 worker if they have more than one job at a time or have a spouse and are jointly filing. Tip: for it to be accurate, the IRS advises the employee to submit a W-4 for all other jobs.

Step 3. Claim Dependents

This section only needs to be completed if the worker has children and is applying for relevant credits related to them.

Step 4. Other Adjustments

The employee will need to include:

- Sources of income from things such as interest, dividends, or retirement

- Deductions they plan to apply for

In step 4, the nonresident person should just write nonresident alien in the blank space before the end of the section.

Step 5. Sign Here

Name, date and signature to complete it.

Why accurate completion matters

J-1 Visa holders may be eligible for tax treaties that could limit or eliminate tax withholdings entirely. It’s crucial that this form be completed correctly. If the W-4 form is not correct, the worker may pay too little tax during the year and face a large balancing payment at the end of the tax year.

As well as this, a missing W-4 form may lead to backup withholding of 28% or 30% NRA rate.

Supporting your employees

Sprintax Calculus supports organizations in accurately completing W-4 forms for each member of your nonresident population.

J-1 visa holders can fill out form W-4 with Sprintax Forms

If you need support in guiding employees through the correct completion of Form W-4, Sprintax Forms helps nonresident employees prepare compliant withholding documentation and apply treaty benefits where available.

We prepare tens of thousands of documents for nonresidents in the U.S. every year, so it’s safe to say we know a thing or two about nonresident tax!

Form 8233

Form 8233 is used by nonresident workers to claim a tax treaty-based exemption from U.S. federal income tax withholding on personal services income.

The form reports the employee’s country of residence, applicable tax treaty article, amount of income claimed as exempt, and citizenship or green card status.

Employers should develop a clear internal process around Form 8233, this means having either payroll or human resources provide the form to the J-1 employee for completion.

If they are unsure, walk them through IRS guidelines for the form as well as the ‘supporting statement’.

Although there is no section for a signature or date on the supporting statements for employees, ensure the employee also signs the supporting statement.

Review form 8233 and once it is ready:

- Submit one copy to the IRS within five days of receiving it from the employee

- Give one copy to the non-resident

- Place the original forms in the person’s file

Form 8233 is valid for the entire tax year after it is given to the employee.

Sprintax Forms helps J-1 visa holders to complete their Form 8233 easily online!

Form W-8BEN

Form W-8BEN has two primary purposes:

1.) To prove nonresident alien status (this is part 1 of the form). This may be required for both tax treaty and non-tax treaty income

2.) If the worker is entitled to tax treaty benefits for Fixed, Determinable, Annual, Periodical (FDAP) income (examples include – scholarship, grant, prize, award, investment income, royalties), it must be described in section 2 of the form.

Sprintax Forms helps J-1 participants to complete form W-8BEN easily online.

Form W-9

If the J-1 participant is considered a resident for tax purposes, they may be required to provide you with a Form W-9.

This form will confirm the employee’s Taxpayer Identification Number (TIN), and is used to ensure that the participant does not have any backup withholding.

Form W-2

The main purpose of a W-2 form is to report wage and salary information along with other taxes withheld from a worker’s paycheck.

At the end of the tax year, when calculating tax and preparing income tax returns, the J1 visa holder will need the withholding amount that you report on the W-2 form.

By subtracting the figure from their tax bill, the J1 employee will know whether to expect a tax refund or if they have to make an additional tax payment.

You should give your J-1 employee their W-2 by 31 January. If they haven’t received it by this date, be sure to contact your employee to discuss giving it to them.

You can find more information about what income is taxable for nonresidents in the U.S. here.

How Sprintax Calculus supports nonresident tax withholding for J-1 employees

Sprintax Calculus has been developed specifically to help payroll departments to easily manage the tax profiles of their nonresident employees on a single, user-friendly dashboard.

Our tool simplifies a number of aspects related to nonresident taxation, including; residency determination, tax treaty eligibility and tax withholding.

Sprintax Calculus will prepare every document your payroll office requires in order to manage the taxation of your nonresidents including forms W-4, W-8BEN and 8233.

Benefits of Sprintax Calculus

- All-in-one solution for corporations with J visa employees

- Cloud-based, secure and automated, nonresident tax solution

- IRS compliance guaranteed

- Advanced reporting tools

- Instant generation of tax forms (such as 1042-S, W-4, W-8BEN and more)

If you would like to learn more about how Sprintax Calculus can support your organization with nonresident tax solutions, you can simply register for a free demonstration.

Here, a member of our team will walk you through our system and answer any of your questions.