Getting to grips with U.S. tax forms is important for when tax season rolls around.

One of the most important forms that nonresidents should know about is Form W-8BEN.

It’s crucial to have a good understanding of this form – especially if you intend to earn income while in the U.S.

So, with that in mind, we have gathered everything you need to know about Form W-8BEN into this guide!

Table of Contents

- What is a W-8BEN form?

- Who needs to fill out Form W-8BEN?

- Claiming tax treaty benefits

- Is Form W-8BEN required?

- How to fill out W-8BEN

- How long is a W-8BEN valid?

- When and where to submit W-8BEN

- When not to use Form W-8BEN

- Should I file Form 8233 or a W-8BEN?

- Should I file Form W-9 or W-8BEN?

- Form W-8BEN vs Form W-8BEN-E – what is the difference?

- Form W-8BEN or W-8ECI

- What happens if the company files incorrectly on my behalf?

- What are the most common mistakes people make on Form W-8BEN?

- Sprintax Forms can help you complete Form W-8BEN easily online

What is a W-8BEN form?

Form W-8BEN is officially known as the “Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting (Individuals).”

It is used by nonresident aliens to claim an exemption or reduction of U.S. withholding tax if their home country has a tax treaty with the U.S.

The usual rate of withholding tax is 30%. Form W-8BEN’s purpose is to reduce or eliminate this withholding tax payment.

Essentially, if you fail to complete a W-8BEN form, you can expect to be taxed at a rate of 30%, even if your home country has a tax treaty with the U.S.!

Who needs to fill out Form W-8BEN?

If you are a nonresident receiving income (except personal services income) in the U.S., you should fill it out.

Nonresident aliens pay U.S. tax at a rate of 30% on income earned from U.S. sources.

However, if you are from a country which has a double taxation treaty with the U.S., you can avail of a reduced tax rate.

To avail of this, you must fill out a Form W-8BEN.

You can complete form W-8BEN online with Sprintax Forms

Claiming tax treaty benefits

The U.S. has more than 65 open tax treaties with countries around the world.

Whether you’ll be able to claim a tax treaty benefit will depend on a number of factors, including:

- The visa you’re on

- Type of income you received

- What you are being compensated for

- The type of organization that is paying you

1. The visa you’re on

Tax treaties typically offer benefits to nonresident aliens, whereas tax residents cannot take advantage of any tax treaty benefits or exemptions available for nonresidents.

Nonresidents

Generally, if you are on an F or J visa, you are considered a nonresident alien for tax purposes. It is only after your fifth calendar year in the United States that you will become resident for tax purposes.

Residents

If you hold a H-1B or O-1 visa and are present in the U.S. for more than 183 days combined from the last three years, you will be considered a resident for tax purposes. You will need to take the IRS’ substantial presence test to determine your tax residency.

To meet this test, you must be physically present in the U.S. on at least:

- 31 days during the current year, and

- 183 days during the 3-year period that includes the current year and the 2 years immediately before that, counting:

- All the days you were present in the current year, and

- 1/3 of the days you were present in the first year before the current year, and

- 1/6 of the days you were present in the second year before the current year.

2. Type of income you received

Income type is a significant determinant of the level of benefit offered by a tax treaty.

Dividends, interest, and royalties

- This type of passive income is usually faced with a flat withholding tax of 30% for nonresidents in the U.S. However, many tax treaties reduce or eliminate this withholding tax rate (e.g. the U.S. – Switzerland treaty reduces the withholding rate to 15%).

Employment income

- Many treaties include a personal services or employment income article that may exempt income from tax in the source country if certain conditions are met (e.g., you are present less than 183 days, and the payor is not a resident or permanent establishment in the source country).

Business profits

- The treaty treatment of business profits often depends on whether the profits are attributable to a permanent establishment in the source country.

- If the permanent establishment exists under treaty definition, profits are generally taxable. If no permanent establishment exists, the treaty may allow for an exemption or limit taxation.

Scholarships

- Many U.S. tax treaties include a “Student” or “Scholarship” article that specifically exempts scholarship and fellowship income from taxation for eligible nonresident students from treaty countries.

3. Nature of services provided

The nature of the services you perform can impact your eligibility for a treaty benefit.

Personal services

- The majority of tax treaties include provisions for wages or compensation from services performed in the source country.

- To qualify, you generally must meet specific conditions, such as being present for fewer than 183 days in the country during the tax year and receiving payment from an employer who is not a resident or permanent establishment in the source country.

Independent contractor or business services

- If you provide your services as an independent contractor or through a business, treaty benefits may depend on whether you have a permanent establishment in the source country.

- Without a permanent establishment, the treaty may exempt your service income or reduce the tax rate. However, if a permanent establishment exists, the income is generally taxable.

4. The type of organization that is paying you

The type of organization that is paying you for your services can impact the application of treaty benefits:

- Government or publicly traded entities: Payments from government entities, tax-exempt organizations, and publicly traded companies usually meet treaty criteria and are therefore more likely to qualify for reduced holding rates.

- Private entities: If the payer is a private entity, treaty eligibility may pass through to the owners or be limited by “Limitation on Benefits” articles. These articles have been designed to ensure that foreign entities only receive treaty benefits if they are sufficiently connected to one of the countries in the tax treaty.

Can you claim multiple tax treaty benefits with W-8BEN?

Generally, you can only claim one tax treaty benefit with each Form W-8BEN.

If you receive more than type of income from a single withholding agent for which you claim different benefits, some withholding agents will require you to submit a separate Form W-8BEN for each different type of income.

Case study: French citizen claiming a tax treaty benefit using Form W-8BEN

Emma is a French citizen in the U.S. on a J-1 visa. She is receiving a scholarship from a U.S. university for her research fellowship and wants to minimize U.S. withholding tax using the U.S. – France tax treaty.

What steps does Emma have to take to do this?

First, Emma must check her eligibility. As a J-1 visa holder, she is considered a nonresident for tax purposes for the first 5 years of her time in the U.S. Furthermore, her scholarship income qualifies under the treaty’s “Student/Scholarship” article.

Therefore, she is eligible for tax treaty benefits.

The next step for Emma is to complete Form W-8BEN, providing her personal information, evidence of her French residency, and the treaty article reference.

Emma then has to submit this to the payer, in this case her university. They can then apply the correct withholding rate of 14%, instead of the typical 30% rate.

By filing the W-8BEN, Emma has avoided excess U.S. tax on her scholarship by taking advantage of existing tax treaties between the U.S. and France.

Is Form W-8BEN required?

Yes, Form W-8BEN must be provided to the withholding agent by nonresident aliens to certify their foreign status and to claim a reduced rate of withholding tax under an income tax treaty (if applicable).

Without this form, the default withholding tax rate on income earned in the U.S. is 30%.

How to fill out W-8BEN

Below, you can see a copy of a W-8BEN.

W-8BEN instructions

You can download Form W-8BEN online.

Part I: Identification of the Beneficial Owner (lines 1 to 8)

This is your personal data section. Enter your legal name exactly as it appears on your passport, your country of citizenship, and your permanent foreign residence address.

Important: Never use a P.O. Box address for Line 3 (you must enter a physical address); the IRS will reject the form automatically.

Provide Taxpayer Identification Numbers (lines 5 and 6a)

To claim tax treaty benefits, you must connect your profile to a tax identity. Enter your U.S. SSN or ITIN on Line 5 if you have one.

Do not forget Line 8 – the IRS will reject the form if your Date of Birth is missing or not formatted in the U.S. style (MM-DD-YYYY).

Part II: Claim of tax treaty benefits (lines 9 and 10)

In section two, you will be asked about your tax treaty benefits with your home country. You should always check to see if you have any applicable benefits rather than assuming that you do.

This is where you legally reduce your withholding tax. You must list the specific treaty article number, the withholding rate percentage you are claiming, and the type of income (e.g., dividends, royalties, or scholarship grants).

Part III: Certification and Signature

In section three, you will be required to sign and date the form to state that all of the information provided is correct.

Note: The IRS requires a physical (“wet”) signature or an authorized, secure electronic signature.

You can complete form W-8BEN easily online with Sprintax Forms.

How long is a W-8BEN valid?

That depends.

Provided none of your details on the form change, your W-8BEN should be valid for up to three calendar years after the completion date.

For example, if you completed a W-8BEN form on 28 March 2025, it will be valid until 31 December 2028.

When and where to submit W-8BEN

Technically, you do not file W-8 forms with the IRS.

Form W-8BEN will be sent by the organization that is making payments to you.

It should then be returned to the company that sent it to you, not the IRS. You won’t need to file it with a tax return.

When not to use Form W-8BEN

Residents in the U.S. should not file Form W-8BEN. Instead, residents should file Form W-9.

Also, you shouldn’t complete form W-8BEN to outline personal service income. For that you’ll need to fill out form 8233.

Should I file Form 8233 or a W-8BEN?

The correct form depends on the type of income you are receiving.

- Form W-8BEN is used for income that is not considered personal services income, such as investment income (e.g., dividends, interest, or royalties);

- Form 8233 is used specifically to claim a tax exemption or reduced withholding rate on personal services income (wages, salary, consulting fees, etc.).

Another key difference is that Form 8233 must be submitted by the withholding agent to the IRS, whereas Form W-8BEN is generally kept on file by the withholding agent and not sent to the IRS unless requested.

What counts as Personal Services Income (PSI)?

Personal services income is money paid for work you personally perform while physically in the U.S. This can include:

- Teaching or lecturing

- Research work

- Consulting or freelance/contract work (e.g., design, coding, writing)

- Performances by actors, musicians, or dancers

- Compensation for athletes competing in U.S. events

- Medical or specialist services

- Any other labor or service-based work performed in the U.S.

If the payment you received is not connected to work you performed (e.g., dividends, royalties, scholarship not tied to work), it would generally fall under Form W-8BEN instead.

You can fill out forms W-8BEN and 8233 easily online with Sprintax Calculus (Forms).

Should I file Form W-9 or W-8BEN?

The form you use depends on your residency for U.S. tax purposes:

| Form | Who should use it? | Purpose |

|---|---|---|

| Form W-9 | U.S. citizens and U.S. resident aliens | To provide your Taxpayer Identification Number (TIN) to the payer so your income can be reported to the IRS. |

| Form W-8BEN | Non-U.S. residents (nonresident aliens) receiving U.S.-source income | To confirm non-U.S. tax residency and to claim a reduced withholding rate under a tax treaty (if applicable). |

Form W-8BEN vs Form W-8BEN-E – what is the difference?

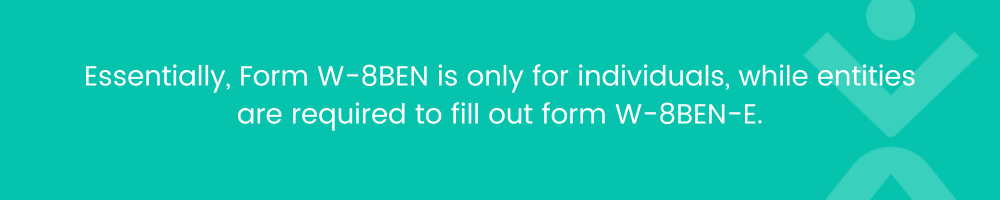

The key difference between these two forms is who they are intended for.

- Form W-8BEN is used by individuals (including sole proprietors or single-owner businesses like independent contractors);

- Form W-8BEN-E is used by entities, meaning any type of business or organization that has more than one owner. They may be corporations, partnerships, exempt entities, foundations (public and private), international organizations, and even foreign governments.

Money received by foreign businesses is also taxed at a 30% rate in the U.S. Much like the W-8BEN, form W-8BEN-E will allow the business to receive a tax treaty deduction if applicable.

Foreign businesses will have to complete this if they earned the same income as listed above.

In truth, there are a few similarities between the two forms, for example the layout and details requested on both of these forms are similar.

Form W-8BEN or W-8ECI

Form W-8ECI, is also known as a “Certificate of Foreign Person’s Claim for Exemption That Income Is Effectively Connected With the Conduct of a Trade or Business in the United States.”

If you are a foreign alien with U.S.-sourced income that is connected to a trade or business in the US, you may file Form W-8ECI to get an exemption from the 30% withholding tax on this income, which is known as ‘Effectively Connected Income’ (ECI).

The exemption applies to income which is effectively connected with a U.S. business or trade, hence the name W-8ECI, which stands for ‘Effectively Connected Income.’

Whereas Form W-8BEN is used by nonresident aliens to claim tax treaty benefits.

What happens if the company files incorrectly on my behalf?

This is a relatively common occurrence, so you shouldn’t panic if it happens.

If this happens, you can simply file a tax return in the US (Form 1040-NR) along with Form 8833 (Treaty-Based Return Position Disclosure Under Section 6114 or 7701(b)) to outline that you are in fact applicable for a treaty.

You should receive a tax refund on any overpayments you may have made shortly after this.

You can also choose to file Form 1040-NR with a tax expert such as Sprintax Returns!

When you use our service, you can finally rest assured you’ll be 100% tax compliant.

What are the most common mistakes people make on Form W-8BEN?

Watch out for these four frequent pitfalls:

Sending the form to the IRS

The IRS does not collect these forms. You must submit your completed W-8BEN directly to the platform, company, or withholding agent paying you.

Leaving Line 10 completely blank while claiming a treaty

If you list your country on Line 9 but fail to specify the explicit treaty article, withholding rate, and income type on Line 10, your withholding agent cannot grant you the lower tax rate.

Using an unaccepted date format

The IRS strictly requires the U.S. date format on Line 8 (Date of Birth) and the signature line: MM-DD-YYYY. Writing it as DD-MM-YYYY is cause for automatic rejection.

Using a P.O. Box for your permanent residence

Line 3 requires your actual physical address. If you enter a P.O. Box address, the form will be flagged as invalid unless you provide accompanying legal proof of residency.

Sprintax Forms can help you complete Form W-8BEN easily online

Are you unsure how to complete W-8BEN form? Sprintax Forms can help you!

We can offer you:

- Online generation of forms, such as W-8BEN, W4, 8233, and more!

- We’ll easily determine your tax residency status thus ensure you are paying the right amount of tax

- Our software will apply every tax treaty benefit you’re due

Our service was created in order to make tax prep easy and ensure our users are fully compliant with the IRS tax rules.