Do nonresident aliens have to pay Social Security and Medicare (FICA) tax?

And what should you do when FICA was deducted from your pay when it shouldn’t have been?

In this guide, we will cover everything a nonresident in the U.S. needs to know about FICA.

What’s the purpose of FICA?

FICA (the Federal Insurance Contributions Act) is the federal payroll tax that funds the two major U.S. social insurance programs: Social Security and Medicare.

These programs provide:

- Retirement benefits

- Disability benefits

- Survivor benefits for children and spouses of deceased workers

- Health insurance for individuals aged 65+ and certain individuals with disabilities.

FICA also provides benefits to children who have lost their working parents, widows and widowers, and disabled workers who qualify for benefits.

For self-employed people, there is an equivalent law called SECA (Self-employed Contributions Act).

How does FICA work?

FICA contributions are automatically deducted from each paycheck. Employees pay one portion, and employers match it.

Your FICA taxes are split between two programs:

- Social Security – retirement, disability, survivor benefits;

- Medicare – health insurance for people age 65+ and certain disabled individuals.

Every time a worker is paid, a percentage of their wages goes toward these programs to support current beneficiaries and secure future benefits for themselves.

What is OASDI tax (on my paycheck)?

OASDI tax is a part of FICA taxes that will be deducted from your payslip.

If you’re an employee in the U.S., 6.2% of your paycheck will go toward OASDI withholding – which helps to fund Social Security.

FICA exemption for nonresident aliens

When are nonresidents exempt from FICA taxes?

Most nonresident aliens in the U.S. do not have to pay FICA (Social Security and Medicare) taxes if they are working under a qualifying visa category or in specific types of student or exchange-visitor employment.

Nonresidents will not have to pay FICA if they are earning income from any of the below employment types:

- On-campus student employment up to 20 hours a week (40 hrs during summer vacations)

- Off-campus student employment allowed by USCIS

- Practical Training student employment on or off-campus

- Employment as a professor, teacher or researcher (within the 2-year exemption period)

- Employment as a physician, au pair, or summer camp worker (within the 2-year exemption period)

Who qualifies for the exemption?

Nonresidents holding the following visa types are generally exempt from FICA as long as they retain nonresident status: F-1, J-1, M-1, Q-1, and Q-2 visas (including students, scholars, teachers, researchers, trainees, physicians, au pairs, and summer camp workers).

FICA exemption for international students

The FICA exemption period covers your first 5 calendar years of physical presence in the U.S. if you are a full-time student at a U.S. educational institution. You are exempt for your first 2 years if you are not a full-time student.

After this period of time has passed, international students are classified as Resident Aliens for Tax Purposes and are subject to withholding of FICA tax.

However, if they remain students (primarily) they may be able to claim the Student Social Security and Medicare exemption.

FICA exemption for students on OPT/CPT

The five-year exemption permitted to F-1, J-1, M-1 full-time students also applies to any period in which the international student is in ‘practical training’ allowed by the United States Citizenship and Immigration Services USCIS, as long as the foreign student is still classified as a nonresident alien for tax purposes.

Оnce the exemption period has passed, this group of nonresidents are classified as resident aliens for tax purposes and subject to FICA tax withholding.

FICA exemption for payments received by students employed by their school

FICA taxes also do not apply to payments received by students employed by a school, college, or university where the nonresident student is pursuing a course of study.

Also read:

When do nonresidents have to pay FICA?

FICA exemption does not apply to:

- Spouses and children in F-2, J-2, M-2, or Q-3 nonimmigrant status

- Nonresidents in employment that is not allowed by USCIS or in employment that is not closely connected to the purpose for which the visa was issued

- Nonresidents in the US on F-1, J-1, M-1, or Q-1/Q-2 visas who change to an immigration status that is not exempt or to a special protected status

- Nonresidents in the US on F-1, J-1, M-1, or Q-1/Q-2 visas who become resident aliens

- If the exempt period has passed – 2 years for J and Q visas and 5 years for F and M students

- The employment should be closely connected to the purpose for which the visa was granted

FICA and residency status

Resident aliens for tax purposes have the same liability for Social Security/Medicare Taxes that U.S. citizens have.

You are considered a resident alien of the U.S. for tax purposes if you meet either the Green Card Test or the Substantial Presence Test (SPT) for the calendar year. Find out more about U.S. residency for tax purposes here.

Green Card Test

If you have a Green Card, you are considered a resident alien for tax purposes.

Substantial Presence Test (SPT)

You will be considered a resident alien for tax purposes if you have been present in the U.S. for at least 31 days in the current year, and present in the U.S. for 183 days over the three-year period that includes the current year and the prior 2 years. The 183 days is calculated as follows:

• Count all the days present in the U.S. in the current year, plus 1/3 of the days present in the U.S. in the first preceding year, plus

• 1/6 of the days present in the U.S. in the second preceding year. If the total is 183 days or more, you have met the SPT and are considered a resident alien.

You can complete the Substantial Presence Test for free with Sprintax.

FICA Tax Rates for 2026

How is FICA calculated?

The FICA tax rate for 2026 for both employers and employees is 7.65% .

This is made up of 6.2% for OASDI (Social Security) and 1.45% for Medicare.

Self-employed workers have to pay 15.3% (12.4% for Social Security and 2.9% for Medicare).

Social Security tax has a wage base limit of $184,500 for 2026 ($176,100 for 2025) – this is the maximum wage that’s subject to the tax. There’s no wage base limit for Medicare tax.

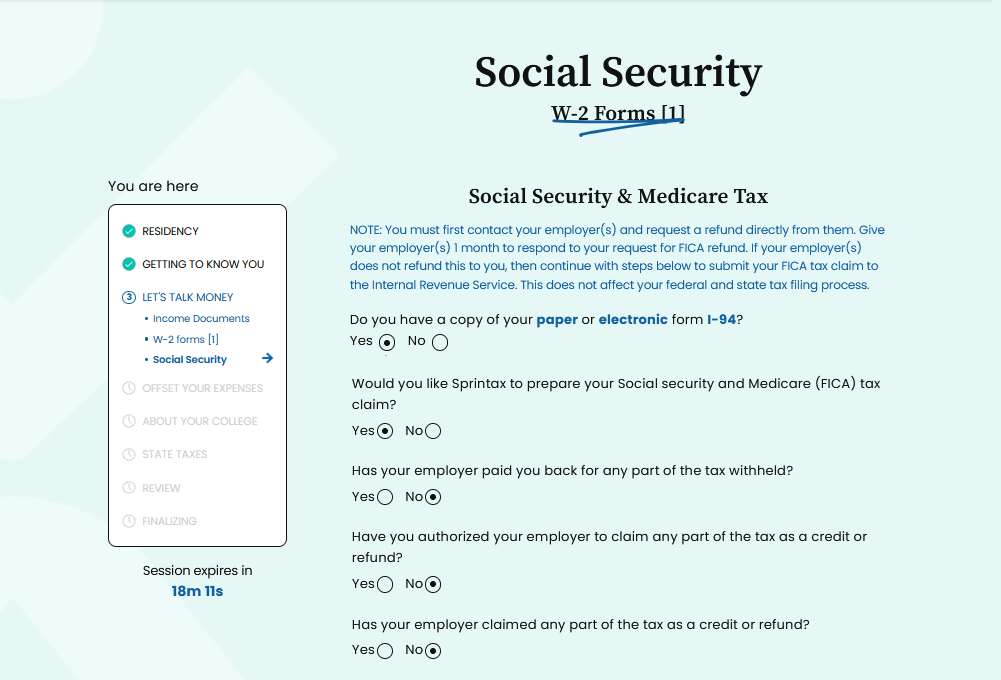

FICA tax refund

If you notice that FICA has been deducted from your pay by mistake, the good news is that you can apply for a refund and claim back your FICA deductions from the IRS.

How do I get my FICA tax refund?

The first thing you need to do is contact your employer and ask for a refund. If a W-2 form was already issued, you should ask for a corrected W-2c for the same year.

If your employer cannot refund you, you still can reclaim it from the IRS.

Sprintax Returns can help you file a FICA tax refund claim

The process is fast and simple. The software will ask you “Would you like Sprintax to prepare your social security and Medicare (FICA) tax claim?”, and you should consent and proceed.

Apply for your FICA tax refund with Sprintax.

How long does it take to get my FICA tax refund?

It will generally take at least 12 weeks for the IRS to process your Social Security and Medicare tax refund, assuming your claim is accepted.

How to check FICA tax refund status

There is no option to check the status of your FICA refund online. You can call the NR department within the IRS: 267-941-1000 (best option is to call at 06:00 AM Eastern time when they open, so you will not be put on hold for a long time) to check the status.