What are tax treaties and how can they help you save money at tax time?

If you’re a nonresident alien in the US, you may be wondering if there are any tax reliefs available which can help you save money on your tax bill. While the answer to this question is likely “yes”, exactly what you will be entitled to will depend on your personal circumstances. The best place to start is by checking whether or not you are entitled to any tax treaty benefits. The US has signed tax treaty agreements with 66 countries around the world and if you are entitled to benefit from one of these agreements, you could potentially save a lot on your taxes. In this guide, we are going to take a closer look at tax treaty benefits – what they are and exactly how you can claim them.Overview

- Countries with a double tax treaty with the US

- US – India tax treaty

- US – China tax treaty

- US – Canada tax treaty

- US – Germany tax treaty

- US – Philippines tax treaty

- US – South Korea tax treaty

- US – France tax treaty

- How to claim tax treaty benefits

- Get help

What is a US tax treaty?

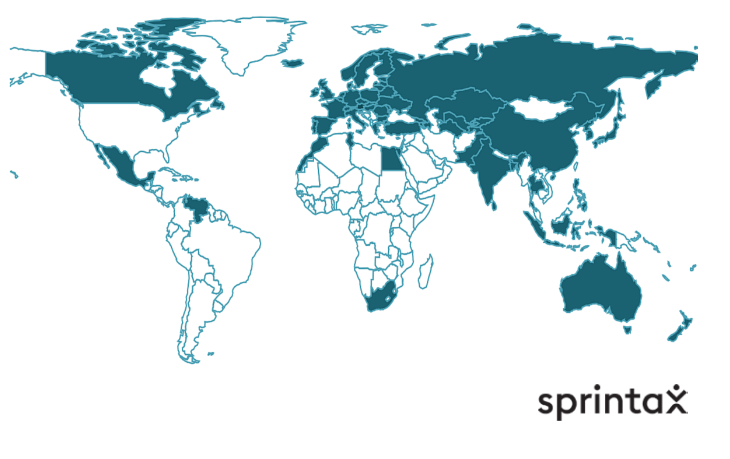

US tax treaties (also known as double taxation agreements (DTA) are specific agreements between the USA and foreign countries that outline how nonresidents will be taxed in each country. Generally, under these tax treaties, residents of foreign countries (including foreign students and scholars) are taxed at a reduced tax rate and can benefit from exemptions on many different types and items of income. That is a great opportunity to save some money so it is really important to ensure that you claim the treaty benefits you are eligible for. IRS Publication 901 (or the tax treaty document itself) will tell you whether a US tax treaty with a particular country offers a reduced rate of income tax for nonresidents.Which countries have a double tax treaty with the USA?

Currently, the US tax treaty network covers approximately 66 countries all over the world, including:

Currently, the US tax treaty network covers approximately 66 countries all over the world, including:

| Armenia | Australia | Austria | Azerbaijan | Bangladesh | Barbados |

| Belarus | Bulgaria | Canada | China | Cyprus | Czech Republic |

| Denmark | Egypt | Estonia | Finland | France | Georgia |

| Germany | Greece | Hungary | Iceland | India | Indonesia |

| Ireland | Israel | Italy | Jamaica | Japan | Kazakhstan |

| Korea | Kyrgyzstan | Latvia | Lithuania | Luxembourg | Malta |

| Mexico | Moldova | Morocco | Netherlands | New Zealand | Norway |

| Pakistan | Philippines | Poland | Portugal | Romania | Russia |

| Slovak Republic | Slovenia | South Africa | Spain | Sri lanka | Sweden |

| Switzerland | Tajikistan | Thailand | Trinidad | Tunisia | Turkey |

| Turkmenistan | Ukraine | Venezuela | United Kingdom | Uzbekistan | Belgium |

Who can claim a tax treaty benefit?

Whether or not you are eligible to avail of tax treaty relief will depend on four factors:- Your visa type

- Your income type

- The type of work you are being compensated for

- The duration of time you are spending in the US

Which types of wages paid to a nonresident alien are exempt under a tax treaty?

The exact type of tax relief you can claim from a double taxation agreement will depend on the treaty that the US has signed with your home country. Below we will take a look at some examples of tax treaty benefits which can be claimed in the US.US and India tax treaty agreement

Below we have highlighted some of the most important articles from the tax treaty that Indian nationals should be aware of.ARTICLE 21 – Payments Received by Students and Apprentices

If you are an international student from India and you are in the US on a student visa (for example, an F-1 or J-1 visa) it is likely that you will not have to pay tax on any grants, scholarships or remuneration from employment – any payment you receive for your maintenance, education or training. Article 21 also enables Indian students and trainees to avail of the standard deduction ($14,600 – for the 2024 tax year). The standard deduction can change from year-to-year) on their income tax return.ARTICLE 22 – Payments Received by Professors, Teachers and Research Scholars

Indian nationals who travel to the US for the purpose of teaching or engaging in research at a university or college will also be ‘tax exempt’ on income earned from these activities for two years from their arrival to the US on this status. Note: this tax treaty is retroactive. If the teacher or researcher stay more than 24 months in the US, they can potentially lose all benefits and may need to pay tax on income which was considered exempt under the tax treaty in previous years.Tax treaty case study (2024 taxation)

Advik Patel arrived in the US from India for the first time on an F-1 visa in 2021. In 2024 he started an OPT (Optional Practical Training) position. As per the requirements of his visa, he is granted permission to work and he has already received his SSN. 1. Residency Advik is considered a nonresident for tax purposes, as he is still in his 4th year on F-1 Visa status. 2. Income Type Advik is working as a researcher as part of his OPT. Wages paid to him are considered compensation during studying and training. 3. Tax Forms Advik does not need to provide an 8233 for the income, which is exempt under the Indian tax treaty. However, he will need to complete a W-4 in the same manner as that of a resident for tax purposes with the same exemptions and allowances. Indian students or apprentices are allowed to use the standard deduction as well as child and other dependent tax credits where applicable (provided they meet certain requirements) At the end of the year, Advik should receive form W-2, but the standard deduction allowance is applied in the calculation of the income tax – just as it would be for a tax resident as it is a condition of the Indian tax treaty. As a nonresident, he is exempt from paying FICA and FUTA taxes. 4. Tax treaty determination Advik can use the standard deduction of $14,600 and resident tax credits where applicable on his 2024 tax return.Determine your tax treaty eligibility easily online with Sprintax.

US and China tax treaty agreement

The US – China tax treaty deals with the double taxation of numerous types of income, including wages, dividends and capital gains. The treaty ensures that no one will have tax withheld at a higher rate than the higher of the two countries’ tax rates, and it also defines where taxes should be paid, which normally depends on where the income arises.ARTICLE 19 – Teachers, Professors and Researchers

Chinese citizens who are in the US for the primary purpose of teaching, giving lectures or conducting research at a university, college, school or other accredited educational institution or scientific are exempt from tax in the US for a period of three years in aggregate.ARTICLE 20 – Students and Trainees

A Chinese student, business apprentice or trainee is exempt from tax (for such period of time as is reasonably necessary to complete the education or training) in the US on:- payments received from abroad for the purpose of his maintenance, education, study, research or training

- grants or awards from a government, scientific, educational or other tax-exempt organization

- income (not in excess of $5,000) from personal services performed in the US

Tax treaty case study (2024 taxation)

Zhang Wei arrived from China on an F-1 student visa for the first time in 2021 and started his OPT in 2024. As per the requirements of his visa, he is granted permission to work and he already received his SSN. 1. Residency Zhang is considered a nonresident for tax purposes, as he is still in his 4th year on F-1 Visa status. 2. Income Type Zhang is working as a researcher as part of his OPT. Wages paid to him are considered compensation during studying and training (income code 20). 3. Tax Forms Zhang must provide Form 8233 for the income that is exempt under the Chinese tax treaty and a W-4 (labeled NRA) for any income paid on top of the first $5,000 that is covered by the tax treaty. Income covered by the tax treaty is taxed at 0% and all other income is taxed at the graduate rate for federal tax purposes. At the end of the year, Zhang should receive two income tax documents – 1042-S with the income covered by a tax treaty and form W-2, if he has income about what is covered by the tax treaty. As a nonresident, he is exempt from paying FICA and FUTA taxes.

4. Tax treaty determination

Zhang can earn up to the first $5,000 in compensation tax-free for studying and training. The tax treaty benefit applies only to such period of time as is reasonably necessary to complete the education or training. Zhang must also be compliant with the requirements of his visa.

US and Canada tax treaty agreement

Article 20 – Students

Canadian citizens who are in the US as international students will be exempt from tax on any US income received for activity related to education, training, or maintenance. Note: any Canadian citizen (including students, trainees, teachers and researchers, and all other visa holders – as long as they are non-residents) can be exempt for up to $10,000 in personal services (OPT, teaching and research are considered personal services) if their total income is under or equal to $10,000. If their income exceeds $10,000, they must pay US taxes on the whole amount. The tax treaty article that covers this type of income is ARTICLE 15 – Dependent Personal Services.

US and Germany tax treaty agreement

ARTICLE 20 – Visiting Professors and Teachers; Students and Trainees

German nationals who visit the US as a professor or teacher at an accredited university, college, school, or other educational institution, or a public research institution will not be subject to US tax on income earned from these activities (for not more than two years from the date of arrival). Meanwhile, German students who are studying in the US can avail of tax treaty benefits on any income they receive related to their training, education or maintenance. German students will also not be taxed on any grant, allowance, or award from a non-profit religious, charitable, scientific, literary, or educational private organization or a comparable public institution they receive in the US. German students will also not be taxed on any income from dependent personal services (includes wages, salaries, fees, bonuses, commissions, and similar designations for amounts paid to an employee) not in excess of $9,000 (for not more than 4 years from the date of their arrival in the US.US and Philippines tax treaty agreement

ARTICLE 21 – Teachers

Where a resident of the Philippines is in the US to teach or engage in research (or both) at a university or other recognized educational institution, their income earned from these sources will be exempt from tax in their first two years (only if their visit is expected to last two years).ARTICLE 22 – Students and Trainees

If a citizen of the Philippines is in the US to study, research or train at a university will not be subject to taxation (in the first 5 years from the date of arrival) on:- Gifts from abroad for the purpose of maintenance, education, study, research, or training

- Grant, allowance, or award

- Income ($3,000 or less) from personal services performed

US and South Korea tax treaty agreement

ARTICLE 20 – Teachers

Korean citizens who are legally in the US for the purpose of teaching or engaging in research will be exempt from tax for income earned from these activities in their first two years, only if their visit is expected to last two years.ARTICLE 21 – Students and Trainees

Korean international students who are in the US to study, train or research at university will be exempt from tax on any grant, allowance, award or income ($2,000 or less) from personal services performed.US and France tax treaty agreement

ARTICLE 21 – Students and Trainees

French citizens who are in the US to study, secure training or research will not be subject to US tax on any income earned from:- Gifts from abroad for the purpose of maintenance, education, study, research, or training

- Grant, allowance, or award

- Income ($5,000 or less) from personal services performed

How can I claim tax treaty benefits?

When you start working in the US, your employer will ask you to fill out some important payroll forms (such as forms W-8BEN and 8233). These forms help to ensure that tax treaty benefits are applied to your income and that the correct amount of tax is withheld. These forms can be tricky to complete, and it’s important to take your time as it is very important that they are completed correctly.How to complete Form W-8BEN?

In order to claim a tax treaty benefit on a non-compensatory scholarship or grant, you must fill out a W-8BEN form. To fill out your Form W-8BEN, you will need to know your:- Name

- Country of origin

- TIN

What is a Form 8233?

If you are an international student and wish to claim a tax treaty benefit on income from personal services, compensatory scholarship or grant receiving, you will need to complete a Form 8233 and submit it to your university. Note: You must complete a separate Form 8233:- For each tax year

- For each withholding agent (University)

- For each income type

- Personal Information e.g. name, TIN, address in your country of residence

- A description of the services provided and the total amount of income earned

- The exact treaty on which you are basing your claim for tax exemption

- The date of your entry to the US and the date that your current non-immigrant status expires

- You may also need a copy of your visa